See How We're Different

or Call Us: 951-547-6770

Why Understanding Displacement Coverage Could Save You Thousands

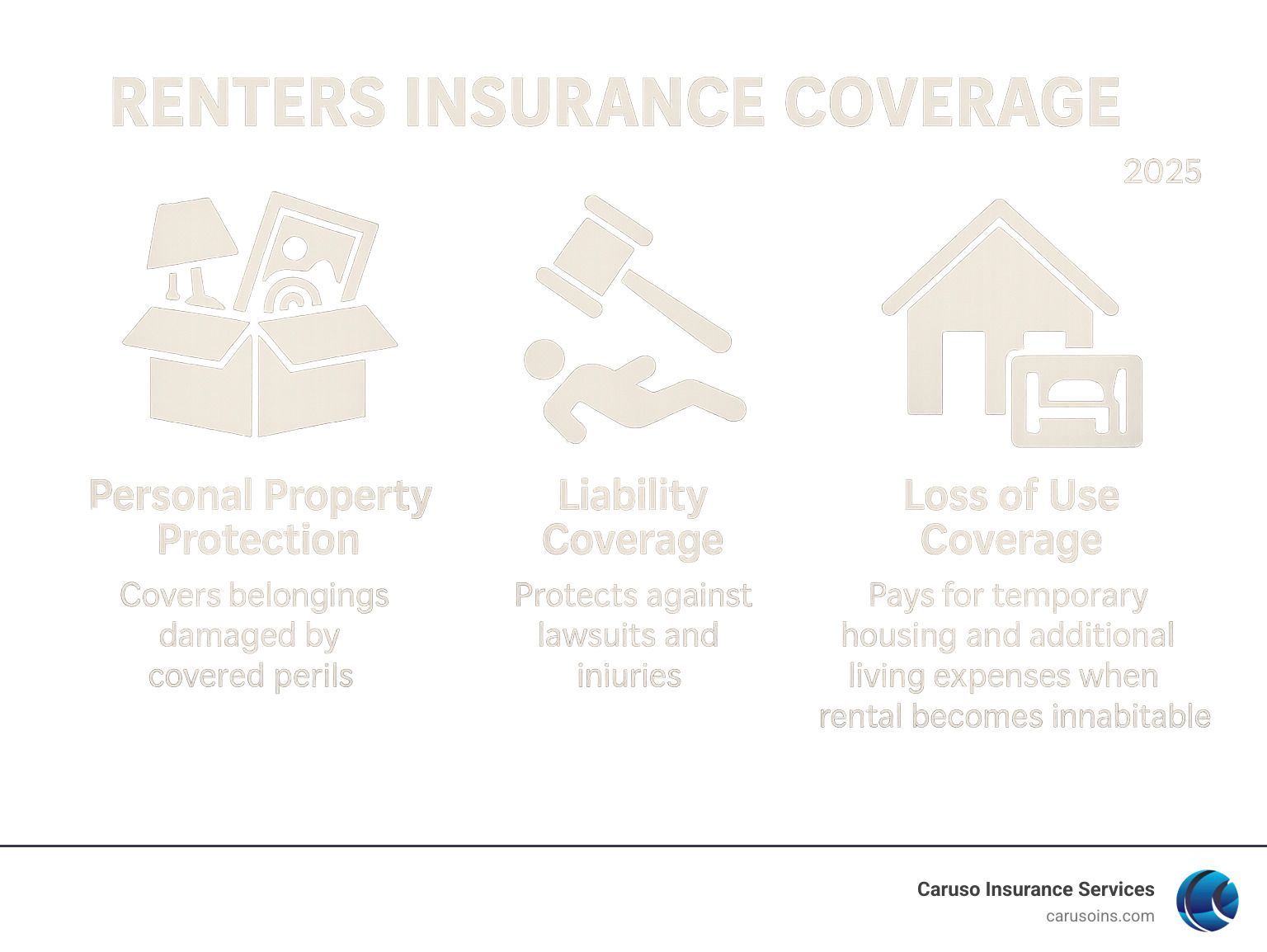

Does renters insurance cover displacement? Yes, most renters insurance policies include “Loss of Use” or “Additional Living Expenses” coverage. This pays for temporary housing and related costs when your rental becomes uninhabitable due to a covered event like a fire, storm, or burst pipe.

Displacement coverage typically includes:

- Hotel stays and temporary rentals

- Increased food costs

- Storage fees for your belongings

- Extra commuting costs

- Laundry expenses

- Pet boarding fees

Coverage limits: Usually 12-24 months or a percentage of your personal property coverage.

Not covered: Floods and earthquakes typically require separate policies. Displacement due to your own negligence may also be excluded.

When disaster makes your rental unlivable, this coverage provides critical financial protection. I’m Patrick Caruso, an independent insurance agent who has helped countless renters in Colorado, Arizona, Florida, Nevada, Texas, Tennessee, and Idaho steer displacement claims and understand their coverage options.

What is ‘Loss of Use’ and How Does it Cover Displacement?

Imagine coming home to find your apartment uninhabitable due to a fire or flood. Where will you sleep tonight? How will you afford a hotel for weeks while repairs are made?

This is when Loss of Use coverage, also called Additional Living Expenses (ALE), becomes your financial lifeline. It’s a standard feature in most renters insurance policies, designed to cover the extra costs of living elsewhere temporarily when a covered peril forces you from your home.

Think of Loss of Use as your policy’s way of helping you maintain your standard of living. It won’t make you rich, but it will cover the increased costs of living somewhere else while your home is being repaired. This protection is invaluable for renters across Colorado, Arizona, Florida, Nevada, Texas, Tennessee, and Idaho, where unexpected events can happen to anyone.

For more comprehensive information, check out our detailed guide: More info about Renters Insurance.

What qualifies as displacement in renters insurance?

Does renters insurance cover displacement in every situation? No. Your rental must be genuinely uninhabitable due to a covered peril, not just inconvenient.

- Structural damage: A storm tears off your roof, a fire damages load-bearing walls, or flooding compromises the foundation.

- Loss of essential services: A fire knocks out your electrical system or a burst pipe leaves you without water. A general neighborhood power outage does not qualify.

- Health and safety hazards: Severe smoke damage, extensive water damage leading to immediate mold risk, or contamination from a covered peril.

- Government evacuation orders: Authorities may prohibit access to your rental due to damage to neighboring properties, which can trigger “prohibited use” coverage.

The key is that the displacement must result from a covered peril that makes it impossible or unsafe to remain in your home.

How ‘Loss of Use’ coverage works for you

Loss of Use coverage is a reimbursement system. You typically pay for expenses upfront and submit receipts to your insurer. It covers increased expenses, not your total living costs. For example, if your rent is $800 and a temporary apartment costs $1,200, your policy would cover the extra $400.

Commonly covered expenses include:

- Hotel stays and temporary rent for accommodations comparable to your original rental.

- Increased food costs if you can’t cook and must eat out.

- Laundry services if you had in-unit facilities and your temporary housing does not.

- Storage fees for your belongings during repairs.

- Extra commuting costs from your temporary home.

- Pet boarding fees if your temporary housing doesn’t allow pets.

The secret to a smooth claim is to keep every single receipt. Meticulous documentation makes the difference.

So, Does Renters Insurance Cover Displacement and Temporary Housing?

Yes, renters insurance does cover displacement when a covered event forces you from your home. This protection comes from your “Loss of Use” coverage, one of the most valuable parts of your policy.

When a burst pipe floods your apartment or smoke from a fire makes it unlivable, your insurance steps in to cover the cost of temporary housing. This could be a hotel for a few nights or a short-term rental for several months while repairs are made.

This coverage kicks in when your rental becomes uninhabitable due to a covered peril, helping you maintain your normal standard of living without paying double for housing during a stressful time.

What specific events can trigger displacement coverage?

Coverage is triggered by a “covered peril”—an event specifically listed in your policy. Common covered events that can force you from your home include:

- Fire and smoke damage

- Windstorms and hail

- Burst pipes and sudden water damage

- Vandalism and theft damage

- Explosions

- Weight of ice or snow

However, some major events are typically not covered by standard policies and require separate insurance:

- Floods from natural disasters

- Earthquakes

- Widespread power outages not caused by damage to your unit

- General pest infestations

Understanding your specific policy is key, and we’re always happy to walk through the details with you.

What types of temporary housing are usually covered?

Your insurance company helps you find temporary housing that is “comparable” to your previous home—not a luxury upgrade, but not substandard either.

- Hotels and motels are common for short-term displacement.

- Furnished short-term apartments are often used for longer stays.

- Vacation rentals are increasingly accepted by insurers for extended displacement.

If you were renting a one-bedroom apartment, your policy will cover a similar one-bedroom unit. It’s wise to communicate with your insurer about your housing choice to ensure it falls within your policy guidelines and prevents reimbursement issues.

Understanding the Financials: Limits, Exclusions, and Extra Costs

Your renters insurance isn’t a blank check, but it is a financial lifeline. It’s crucial to understand the limits and what’s covered.

The key concept is “additional living expenses.” Your policy covers the extra costs you face due to displacement, not your total living expenses. You are still responsible for your regular rent, but insurance covers the hotel bill, increased food costs, and other new expenses.

| Covered Additional Living Expenses (Examples) | Non-Covered Expenses (Examples) |

|---|---|

| Hotel/Motel/Short-term rental stays | Mortgage on a new home (unless it’s your new primary residence post-displacement) |

| Increased food costs (eating out) | Luxury upgrades to temporary housing (e.g., significantly larger or more expensive than original) |

| Storage unit fees | Rent on the damaged unit (your normal rent is still due) |

| Extra commuting costs | Voluntary relocation expenses (e.g., moving for a new job) |

| Laundry service fees | Costs associated with permanent relocation (e.g., moving truck for a final move) |

| Pet boarding fees | Damages from uncovered perils (e.g., natural floods, earthquakes) |

This distinction is vital for budgeting during your displacement.

Are there limits on temporary housing coverage?

Yes, every policy has limits. These are typically set in two ways:

- Dollar Amount Limit: This is either a specific sum (e.g., $10,000) or a percentage of your personal property coverage. For example, 20% of a $30,000 personal property limit would provide $6,000 for displacement costs. Hotel stays, meals, and storage fees add up quickly, so ensure your limit is adequate.

- Time-Based Limit: Coverage is usually capped at 12 to 24 months. It ends when your home is repaired, you find permanent new housing, or you reach your policy’s time or dollar limit, whichever comes first.

Renters insurance is affordable, often just $12-20 monthly, while being displaced without it can cost thousands. Learn more at our Average Cost of Renters Insurance page.

What common situations are NOT covered?

Understanding exclusions can save you from surprises. Coverage is generally not provided for:

- Widespread power outages: If the outage doesn’t stem from physical damage to your unit, it’s not covered.

- General pest infestations: Bed bugs or roaches are considered maintenance issues, not covered perils.

- Mold from neglect: Gradual mold growth is excluded. Mold from a sudden, covered event (like a burst pipe) may be covered.

- Flood and earthquake damage: These require separate, specific insurance policies.

- Intentional acts: Damage you cause intentionally or through gross negligence will likely be denied.

- Voluntary moves: Relocating for a new job or personal preference is not covered.

Does renters insurance cover displacement for pet accommodations?

Yes, most Loss of Use coverage extends to reasonable pet-related expenses. If your temporary housing doesn’t allow pets, pet boarding fees at a standard kennel are typically covered as an additional living expense. Keep all receipts for these costs, just as you would for your own expenses. For more on pet-related coverage, see our guide on

Dog Bites and Homeowners Insurance.

How to File a Claim for Temporary Housing Expenses

At Caruso Insurance Services, we’ve guided clients across Colorado, Arizona, Florida, Nevada, Texas, Tennessee, and Idaho through this process. The key is to act fast, document everything, and keep every receipt. You are seeking reimbursement for additional living expenses—the costs you have only because you were displaced.

What steps are needed to file a displacement claim?

Follow this roadmap after a covered disaster:

- Contact your insurance company immediately. Use their 24/7 claim hotline. The sooner you report it, the sooner they can help.

- Get to safety first. If your rental is unsafe, leave. Your insurer would rather pay for a hotel than an injury claim. For guidance on next steps after a disaster, resources from the American Red Cross can be very helpful.

- Document the damage with photos and videos. Before any cleanup, capture images of what made your home unlivable. This is crucial evidence.

- Save every receipt. Start a physical or digital folder for all expenses: hotel stays, meals, laundry, etc.

- Keep detailed records. A simple spreadsheet listing the date, cost, and reason for each expense will help ensure you get fully reimbursed.

- Fill out claim forms completely and accurately. Rushing can lead to delays.

- Stay in contact with your insurance adjuster. Be responsive and honest. They are there to help process your claim based on your coverage. For more on specific issues, our guide on If a Pipe Breaks may be useful.

What documentation will you need?

Thorough documentation is your best friend during a claim. Gather the following:

- Photos and videos of the damage showing why the home was uninhabitable.

- Receipts for all temporary housing, including hotel bills or rental agreements.

- Receipts for food expenses, especially if you cannot cook.

- Storage unit contracts and receipts if you must store belongings.

- Records of extra transportation costs, like mileage logs or public transit receipts.

- Receipts for laundry if you don’t have access to a washer/dryer.

- Pet boarding receipts if your temporary housing is not pet-friendly.

- A log of all communications with your insurance company.

The golden rule: When in doubt, save the receipt.

Landlords, Tenants, and Why Insurance is Non-Negotiable

If your apartment floods, who pays for your ruined belongings and hotel? Many renters mistakenly believe their landlord’s insurance will cover them. It won’t.

Landlord insurance protects the building structure and the landlord’s liability. It does not cover your personal belongings or your living expenses if you’re displaced. That protection comes from your renters insurance policy’s Loss of Use coverage.

Your landlord’s policy protects their investment (the building); your policy protects your life inside it. For landlords, requiring renters insurance is a smart business practice. When tenants have their own coverage for displacement costs, it reduces disputes during stressful situations.

From a cost-benefit perspective, renters insurance offers incredible value. For a small monthly fee, you get protection that could save you thousands. Learn more about typical costs here: Apartment Insurance Cost.

What happens if you’re displaced but don’t have renters insurance?

Without renters insurance, you are on your own financially. Every dollar for hotels, meals, and storage comes directly from your pocket, with no reimbursement.

These out-of-pocket expenses add up fast. A hotel can cost $100-150 per night, and restaurant meals another $50-75 daily. This financial hardship can quickly drain your savings, especially if displacement lasts for weeks or months. You are left in complete self-reliance mode, scrambling for housing while dealing with the stress of a damaged home and potential disputes with your landlord.

The monthly cost of renters insurance is typically less than one day of displacement expenses.

Can landlords in Colorado, Arizona, Florida, Nevada, Texas, Tennessee, or Idaho require you to have it?

Yes, landlords in these states can and often do require renters insurance as a condition of the lease agreement. This isn’t to be difficult; it’s a practical measure.

Requiring insurance provides benefits for landlords. Your liability coverage protects them if you accidentally cause damage, and it reduces their overall risk. It’s also a form of tenant screening, as it shows you are a responsible renter. This has become common practice in the rental market.

Your landlord may ask to be listed as an “interested party,” which simply means they are notified if your policy is canceled. View this requirement as a benefit: your landlord is ensuring you have the financial protection you need.

Does Renters Insurance Cover Unexpected Displacement?

So, does renters insurance cover displacement? The answer is a resounding “yes!” thanks to your policy’s “Loss of Use” or “Additional Living Expenses” coverage. This feature is a financial shield, stepping in to cover the extra costs you face when a covered disaster like a fire or burst pipe makes your home unlivable.

It helps pay for hotels, increased meal costs, storage, and even pet boarding while you’re displaced. We’ve learned that knowing your policy’s limits and keeping excellent records are key to a smooth claim.

The small monthly cost of renters insurance—often just $12 to $20—is a tiny investment compared to the thousands of dollars you could face in an emergency. It provides peace of mind, allowing you to focus on getting back to normal instead of worrying about money.

At Caruso Insurance Services, we craft policies that fit your unique life, providing comprehensive coverage. We’re here to help you find the perfect renters insurance to protect your belongings, cover your liability, and provide a temporary home when you need it most. Don’t wait for disaster to strike. Protect your future today.